Approval Doesn't Equal Delivery

The Week Housing Policy Met Market Reality

This week’s housing story was not one headline.

It was a contradiction.

Rates are rising.

Approvals are falling.

Investors are still borrowing.

Battery uptake is surging.

Governments are still promising housing supply.

On paper, Australia is trying to build its way out of the housing crisis.

In reality?

The market is asking a much harder question: can these projects actually be delivered?

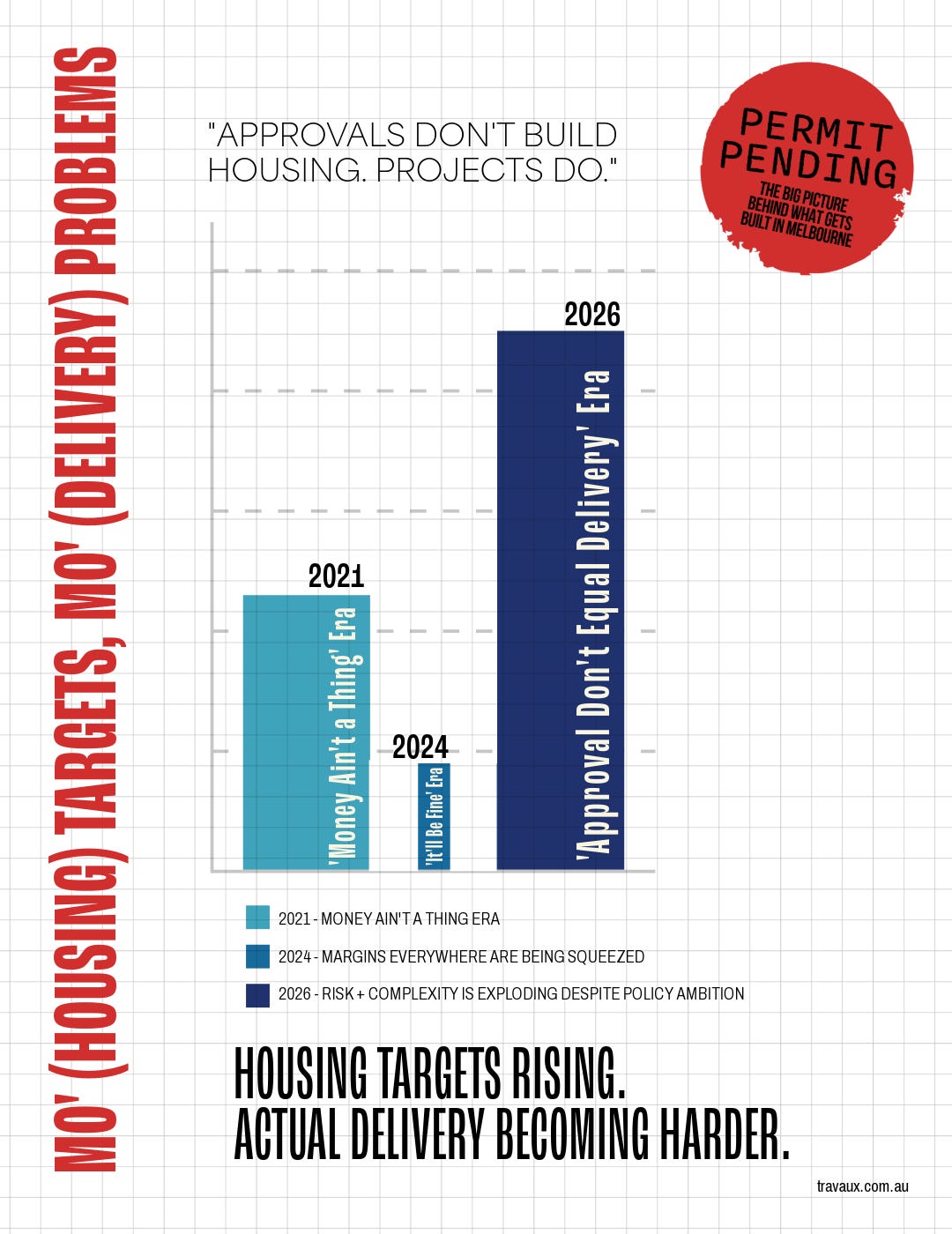

Australia doesn’t just have a housing shortage

It has a delivery mismatch.

This week, building approval data showed a familiar pattern emerging again: detached houses held up reasonably well, while unit approvals softened sharply.

And that matters.

Because the exact housing typologies governments are now aggressively pushing - apartments, density, infill and higher-yield projects - are also the projects under the most financial pressure.

Not because people don’t need housing.

But because:

construction costs remain elevated

debt is expensive

infrastructure competition is tightening labour

buyer confidence is selective

and exit risk is becoming harder to ignore

Approval does not automatically equal delivery.

That’s the gap the industry keeps running into.

Rates are no longer just a borrower problem

The latest interest rate rise matters far beyond mortgage repayments.

For developers and project teams, rates now affect:

acquisition assumptions

holding costs

debt servicing

buyer borrowing capacity

sales velocity

and overall project risk

The market is no longer reacting to rates emotionally.

It is reacting structurally.

A rate rise now changes:

what sites are worth

what products are viable

and whether projects proceed at all

That is a completely different phase of the cycle.

The market isn’t collapsing. It’s splitting.

One of the more interesting signals this week was the contrast between:

stronger investor borrowing activity

and softer broader buyer sentiment

This is not a uniform market anymore.

Sophisticated investors and better-capitalised players are still moving.

But the middle is tightening.

Clearance rates remain softer. Buyers are more selective. Lending buffers matter more. Product mismatch is being punished faster.

The market has not stopped.

It has become far less forgiving.

This is not a crash story.

It is a selectivity story.

Energy is quietly becoming a development issue

One of the less discussed stories this week was the acceleration in battery uptake and renewable infrastructure investment.

At first glance, this feels disconnected from housing.

It isn’t.

Energy resilience is increasingly becoming:

a buyer consideration

a construction consideration

and eventually, a feasibility consideration

Battery rebates continue to accelerate uptake, while major players like Amazon are signing enormous renewable and storage agreements to secure long-term energy reliability for Australian operations.

That matters because:

power pricing volatility affects operating costs

infrastructure demand affects construction inputs

and energy resilience increasingly influences buyer expectations

The next phase of residential development is not just about density.

It is increasingly about:

resilience, efficiency and operational certainty.

Melbourne is entering a more disciplined phase

Melbourne’s market still has long-term structural demand:

population growth

migration

undersupply

infrastructure investment

None of that disappears overnight.

But the market is clearly becoming more disciplined.

Projects that still work are generally:

well located

tightly designed

commercially realistic

aligned to actual buyer demand

The era of relying on endless uplift, aggressive assumptions or “the market will catch up later” thinking is fading.

And honestly?

That may not be a bad thing.

Where this hits your project

Acquisition

Rates and softer buyer sentiment are changing what sites are worth and what risks the market will tolerate.

Planning

Approvals alone are no longer enough. The project still needs to stack under current market conditions.

Design

Product-market fit matters more than ever. Overspecification and poor buyer targeting are becoming expensive mistakes.

Construction

Fuel, labour, infrastructure pressure and energy costs continue feeding uncertainty into delivery assumptions.

Sales & Exit

Buyers still exist - but they are more selective, more constrained and slower to move.

Final thoughts

This week reinforced something the market is slowly starting to understand.

The housing conversation is no longer just about supply.

It is about:

feasibility

timing

delivery risk

infrastructure pressure

buyer capacity

and project resilience

Governments can push targets.

Councils can approve density.

But eventually every project still runs into the same question:

Does it actually work in the real market?

And increasingly, that answer is becoming more complicated.

What are you seeing on the ground?

Are projects becoming harder to deliver - or simply more selective?

Rebecca Lloyd-Jones is a development strategist and founder of Travaux, working across the intersection of planning, construction, market dynamics and project delivery.

Through Permit Pending and Site Intel, she analyses the forces shaping residential development in real time – from interest rates and planning policy through to construction costs, infrastructure pressure and delivery risk – translating them into clear, practical insights across the full project lifecycle.